演講時間:113年12月3日下午1點30分

演講地點:A813

講題: Unrolling Reweighted Parsimonious Features for Trading

摘要:

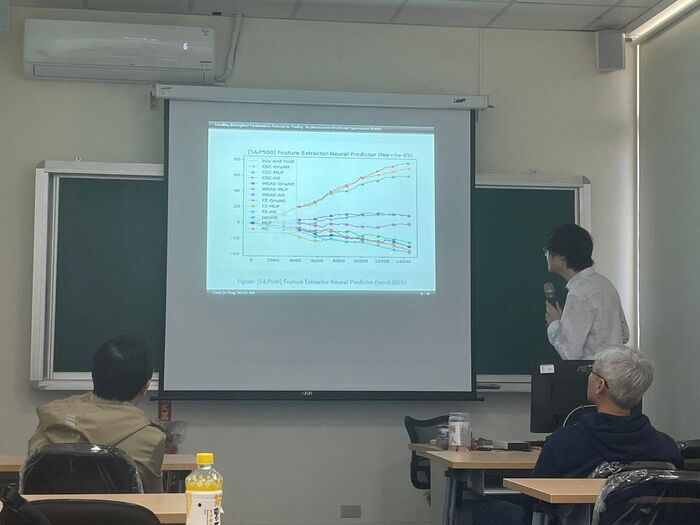

Deriving informative features from noisy signals delivered by the markets is consequential to applying machine learning in trading tasks. Using technical indicators introduced by financial engineering or signal processing as the features fail to fit into the target task data due to their deterministic calculating methods. Learning feature descriptors from data may dictate relevant features, but the noise within the fetched signals can misguide the learning procedure and thus hinder the application's performance. To solve this problem, we proposed to obtain the features using the parsimonious representations of input signals, which were proven promising regarding de-noising images and audio. Deriving such representations is formulated as the convolutional sparse coding (CSC) with the L0 regularization function. Then, we unroll a non-convex, non-smooth proximal splitting algorithm that solves the CSC to construct a recurrent neural network as the feature descriptor. In addition, we proposed a novel boosting method named profit boost that ensembles multiple machine learning models to enhance the performances of trading tasks further. We also proposed a general learning framework that allows our feature descriptor and boosting method to consider numerous input signals from different sources. The experimental results demonstrate that the trading strategy provided by the proposed methods significantly outperforms the prior ones derived using machine learning regarding trading profits and stability.

活動海報與照片: